"B2B BNPL" is a Borrowed Label: Why B2B Platforms Offering Net Terms Need Infrastructure

Buy Now Pay Later made a lot of sense for consumers. Klarna, Affirm, and Afterpay built real businesses by inserting a financing moment at checkout. D2C transactions include a single buyer, a single purchase, a decision made in seconds. The model worked because it mapped cleanly to how consumer transactions actually happen.

Then B2B fintechs borrowed the label.

"B2B BNPL" started appearing in pitch decks and product pages around 2021. Companies like Slope and Resolve adopted the phrase because it communicated the core idea that most people deferred payment for business buyers: written in language investors and buyers already understood.

The problem is that the label imports a set of assumptions that don't hold in most B2B contexts. The right construct isn't B2B BNPL for platform operators trying to build payment infrastructure that actually works across freight and logistics, healthcare, contingent workforce, AP automation, and most of B2B trade. Platforms need infrastructure that facilitates net payment terms: a payment coordination layer that embeds into existing approval workflows, handles both sides of the transaction simultaneously, and reconciles automatically.

That distinction matters more than it might appear. The gap between a checkout-layer BNPL product and embedded net terms solution is the difference between a narrow feature and a compounding platform moat.

Where "B2B BNPL" Came From

The consumer BNPL boom peaked around 2021. Klarna was valued at $46 billion. Affirm went public. Afterpay sold to Square for $29 billion. The model was simple, legible, and generated enormous transaction volume.

B2B fintech companies were raising money in the same environment. Slope closed a $30 million Series A in 2022 using some version of "B2B BNPL" in their positioning, because it was the fastest path to a category investors already had conviction in.

That was a rational fundraising decision. It is not a product architecture decision.

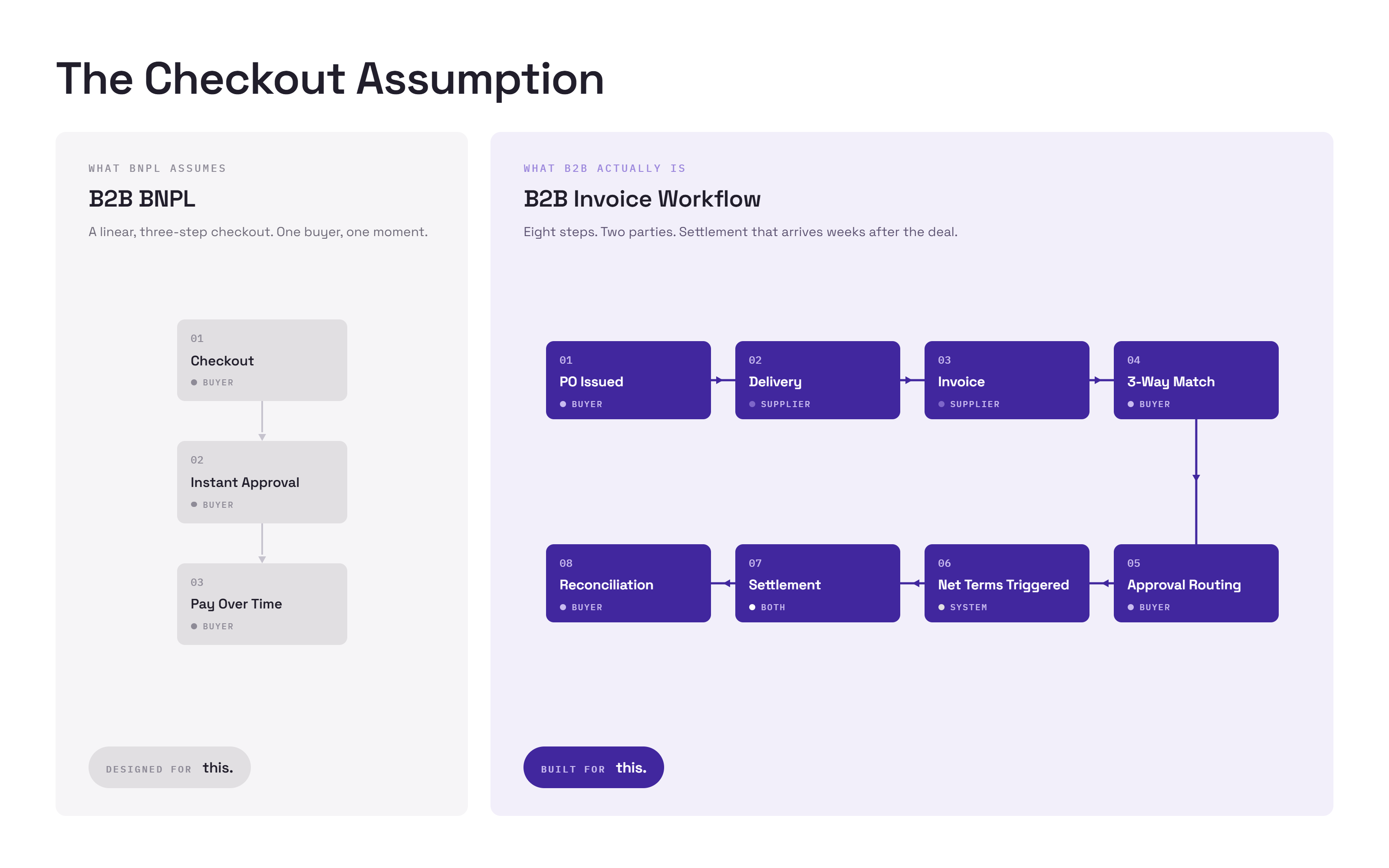

Consumer BNPL was built around a specific moment: a buyer at checkout, choosing to split or defer a payment before completing a purchase. The entire product experience including application, approval, and repayment is organized around that moment. It happens once, for one party, at one point in time.

B2B commerce doesn't work this way. Payment decisions are downstream of a multi-step process: purchase orders, delivery confirmation, invoice generation, three-way matching, approval routing, and sometimes dispute resolution. In B2B trade, there is no checkout moment. The BNPL frame was designed for the 20% of B2B commerce where one exists.

What B2B BNPL Providers Actually Do – and Where They Stop

To be fair: companies like Slope and Resolve built real products that solve a real problem for a specific type of merchant.

Slope Pay integrates at checkout for B2B e-commerce and wholesale platforms. A business buyer places an order, selects to pay later at checkout, and Slope underwrites and funds the transaction. Resolve operates similarly but primarily in wholesale and distribution contexts.

The honest case for B2B BNPL: it is fast to implement, requires minimal integration lift, and works well for catalog-based or portal-based purchasing where a checkout moment exists. For a wholesale distributor selling through a branded storefront, either product is a reasonable option.

Both products are fundamentally supplier-initiated, buyer-side financing tools. The platform integrates B2B BNPL. The buyer gets a payment option at checkout. Rarely do they have visibility into the buyer's AP system. Neither sees both sides of the transaction simultaneously.

When a B2B BNPL payment settles, someone still has to manually match that settlement to the original invoice in the supplier's accounting system. The reconciliation problem – one of the most expensive operational burdens in B2B trade – goes untouched. You've replaced one problem with two workflows.

Resolve's own blog positions B2B BNPL primarily for "merchants who sell to other businesses." That framing is accurate. It also reveals exactly how narrow the use case is. It was designed for merchants with storefronts, not platforms with multi-step invoice workflows. And it definitely was not designed for AP automation, freight and logistics, contingent workforce, or any vertical where the payment moment lives at the end of a complex operational process.

The Vertical Problem: One Size Fits None

B2B BNPL providers offer a largely standardized product. That standardization is part of what makes them fast to implement. It's also what limits them.

The structural failure of B2B BNPL is that it assumes there's a discrete point in time where a buyer makes a purchase decision and can be offered payment options.

That moment exists in maybe 20% of B2B commerce.

In the other 80%, payment decisions are the end product of a multi-step process that looks nothing like a consumer checkout.

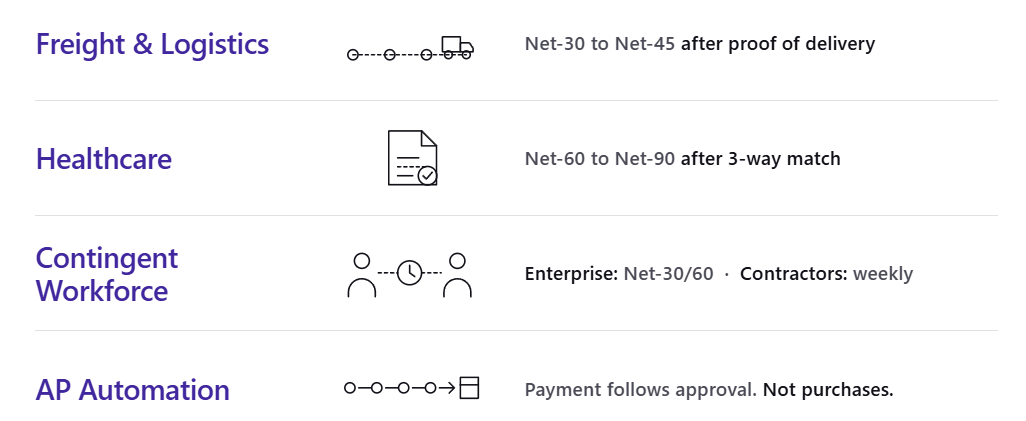

Freight and Logistics. A shipment generates a rate confirmation, a bill of lading, tracking data, an invoice with accessorial charges (detention, fuel surcharges, layover fees), and potentially a dispute – before payment terms are even triggered. Terms are negotiated per load or per carrier relationship. Settlement follows proof of delivery. The cash flow problem here isn't a buyer deferring at checkout; it's a carrier that needs to be paid on delivery and a shipper operating on Net-30.

Healthcare. Hospital procurement runs on Net-60 to Net-90, driven by reimbursement cycle dependencies and multi-level approval hierarchies. A single medical supply invoice may require sign-off from department heads, supply chain managers, and finance.

Contingent Workforce. Enterprise clients on staffing or EOR platforms operate on Net-30 to Net-60 while the contractors they engage expect weekly or bi-weekly pay. The platform sits between those two timelines, absorbing the float or enforcing "pay-when-paid" models that damage contractor retention. Solving this requires the platform to extend credit to the enterprise buyer while immediately funding contractor payouts.

AP Automation. Invoice approvals on platforms like AvidXchange, Tipalti, or Coupa route through configurable multi-step workflows before any payment instruction is issued. By the time a payment is authorized, the invoice has been matched against a purchase order, approved by multiple stakeholders, and scheduled. The payment moment is the conclusion of a process. Net terms infrastructure connects to that process.

Uptake Numbers Tell the Real Story

The architectural difference between checkout-layer BNPL and workflow-embedded net terms infrastructure shows up most clearly in adoption data.

Virtual card programs typically achieve 5% to 15% supplier acceptance in B2B ecommerce contexts. Enterprise suppliers and manufacturers routinely decline card acceptance to avoid 2% to 3% processing fees.

The OatFi network bears this out. Some partner platforms see net terms uptake of 15–35% across enterprise, mid-market, and SMB end users. In industries with structurally adverse payment terms like wholesale trade, manufacturing, and construction, utilization rates for embedded net terms solutions run 45–60%.

Embedded financial products that live inside the platform's native workflow show materially different adoption patterns. Adyen's 2024 Embedded Finance Report found that platforms offering financial services natively inside their software see up to 2x higher product activation rates compared to redirect-based or third-party-checkout approaches.

The churn data tells the same story from a different direction. Platforms that embed financial services into their core workflows see roughly 20% lower gross revenue churn than software-only competitors, according to William Blair's analysis of embedded finance adoption across SaaS platforms.

What Net Terms Actually Means

Net terms extend beyond financing. The liquidity through funding is a component. Infrastructure is needed to coordinate both sides of a B2B transaction, inside the platform's existing workflow.

The distinction matters because most "B2B financing" products only address one side of the transaction. They extend payment timing for the buyer but don't necessarily guarantee payment timing for the supplier. They don't reconcile automatically into either party's system. They don't connect to the buyer authorization event that already exists inside the platform's workflow.

This working capital infrastructure, built correctly, does all four things simultaneously:

It connects to the platform's native authorization event. Invoice approval on an AP platform. Proof of delivery on a freight TMS. Timesheet sign-off on a contingent workforce platform. The financing logic is triggered by the event the platform already uses, not by a new checkout surface layered on top.

It handles both sides of the transaction at once. Buyers get extended payment terms. Suppliers get payment certainty: either guaranteed payment on the due date or early payment on demand. The platform doesn't have to choose which side to solve for.

It creates incentives for on-time transactions. Workflow flexibility allows platforms to offer buyers rewards for on-time payment, allowing for increased uptake and viral growth.

It reconciles automatically into AP and/or AR systems. Settlement data syncs without a manual matching step. The payment event and the reconciliation event are the same event.

It sits inside the platform, not on top of it. Buyers and suppliers interact with the payment product as a native feature of the platform they already use. There's no redirect, no separate portal, no new workflow to learn.

None of this describes a checkout experience. It describes core infrastructure built directly on top of B2B payment rails. That's the category distinction B2B BNPL providers consistently blur.

Why Net Terms Depth Drives Buyer-Supplier Relationship Quality

B2B BNPL products that operate as a checkout layer outside the core workflow create a rigid experience. Settlement data from the BNPL provider has to be manually matched back to invoices in the supplier's AR system. Payment status isn't visible inside the platform where the invoice originated. Disputes require coordination across multiple systems that don't share a common data layer.

Atradius data puts a number on the problem: 43% of U.S. B2B invoices are currently past due, and the firms reporting the most significant late payment issues cite reconciliation complexity and payment status opacity as primary contributing factors. Truly embedded workflows reduces that opacity by embedding settlement directly into the invoice workflow addresses the root cause.

The relationship flywheel runs in both directions. Suppliers receiving predictable, on-time settlement through a platform's native workflow are more likely to route all their invoicing through that platform, increasing buyer coverage. Buyers with consolidated payment status across their supplier base in a single interface are more likely to approve invoices faster. Faster approvals enable faster settlement. Better settlement data reduces disputes.

What Platform Operators Should Actually Be Evaluating

The "B2B BNPL" label leads platform operators toward the wrong evaluation questions. When the question is "which B2B BNPL provider should we integrate," answers cluster around implementation speed, merchant fees, and buyer approval rates.

The more useful questions:

Does it connect to your existing transaction workflow, or require a new checkout surface? If users have to encounter a new payment step they didn't have before, adoption will be suppressed regardless of how good the product is.

Does it coordinate both sides of the transaction simultaneously? Buyer-side net terms without supplier-side early paymeans your suppliers still don't know when they're getting paid. That uncertainty drives supplier churn and off-platform invoicing.

Does settlement reconcile automatically into your system? If your team or your customers' teams are manually matching settlements to invoices, you've traded one operational problem for another.

Does it work across your customer base, or only at catalog checkout? If your customers include enterprise buyers with complex procurement workflows, freight operators, or healthcare systems, a checkout-layer BNPL product won't work.

The evaluation is "checkout-layer financing versus workflow-embedded infrastructure." Those are different products with different adoption profiles, different relationship dynamics, and materially different long-term retention effects.

What This Looks Like in Practice

OatFi's B2B credit network is built as infrastructure for B2B platforms. It's an integration into the workflow where invoices already originate and get approved.

Platforms that offer net payment terms directly into their payment workflows see adoption rates that reflect the native integration. Order.co embedded OatFi's working capital infrastructure directly into its AP and procurement workflows and built supplier stickiness as a direct function of the payment certainty the infrastructure delivered.

B2B BNPL is not the answer. It's a consumer label applied to a narrow use case in a much larger market. The platforms that will define B2B payments over the next decade are the ones building into the workflows their customers already live in – not bolting a checkout layer onto processes that don't require a checkout.

Plug into OatFi's modern credit network for B2B payments. Talk to OatFi →

Explore how OatFi partnered with these businesses

Ready to get started? Get in touch.